Most recent Economic Perspectives for Central and Eastern Europe

Monetary vigilance amidst industrial resilience in Czechia

Despite Czechia’s successful disinflation in early 2026, the central bank refuses to budge until core inflationary pressures are decisively quelled. The policy stance of the CNB has been among the most conservative in the region, prioritizing the credibility of the 2% inflation target over immediate growth stimulation (our forecast for Czech real GDP growth is 2.1% for both 2026 and 2027).

In March the CNB decided unanimously to keep the policy rate at 3.5 %, maintaining the status quo since May 2025. This decision came despite headline inflation reaching a new nine-year low of 1.4 % in February 2026, and amid heightened uncertainty over the global impact of the war in Iran.

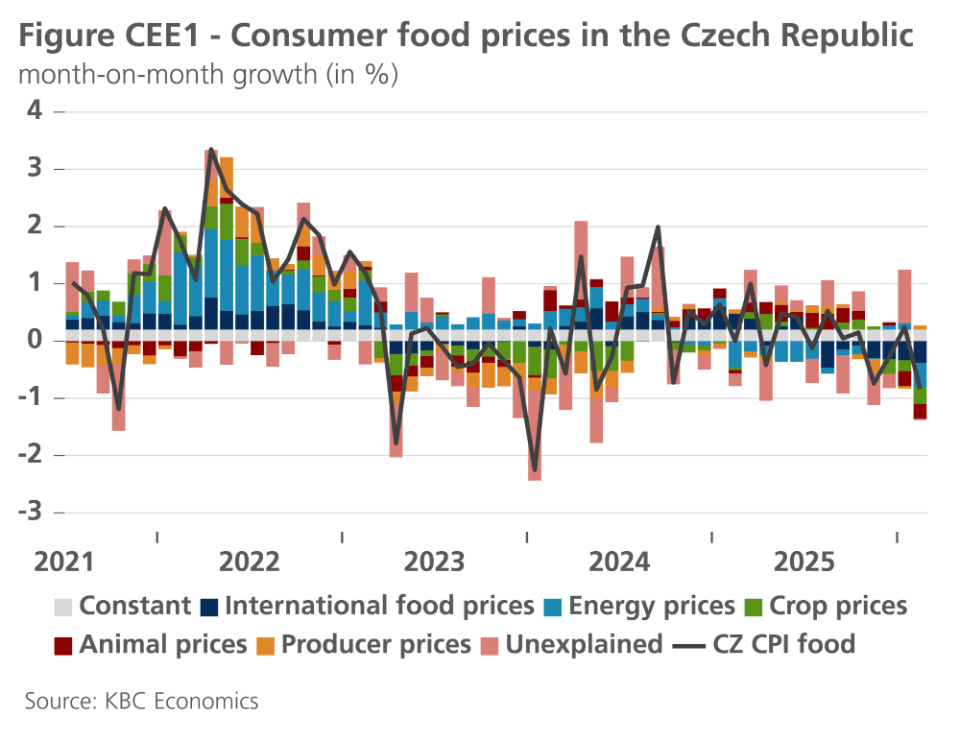

The Board’s reasoning has been centred on the “momentum of core inflation” particularly within the services sector, which remained stubbornly elevated at 4.3% year-over-year in February. While energy and food prices provided a significant downward pull, service sector costs driven by robust nominal wage growth continue to pose a risk. Food prices surprised many on the downside; however, given the recent downward trend in international food prices, government measures in the energy market, and observed declines in agricultural prices, this was broadly in line with our expectations (see Figure CEE1).1 Nonetheless, following the energy crisis, higher energy prices and fertilizer costs can be expected to pull food inflation away from its current downward trajectory. Given the recent increase in energy prices, we should consider the risk of an additional upward pressure of roughly 0.4% in monthly food price growth for the remainder of the year relative to a scenario without the energy shock. The CNB decision to hold rates in March reflects a broader strategy of "wait-and-see" regarding the government's fiscal trajectory and the strength of the koruna. We expect Czech average HICP inflation to reach 1.9% this year and 2.9% in 2027.

Industrial production data indicate that the Czech manufacturing sector is exiting its period of stagnation, albeit with significant sectoral disparities. In January 2026, industrial output rose by 2.8% year-on-year, primarily thanks to the automotive industry.

The Czech labour market continues to exhibit extreme tightness, even as seasonal factors pushed the unemployment rate to 5.2% in February, its highest level since early 2017. Structural changes are leading to increased female labour force participation and a gradual shift of employment from manufacturing to services. Nominal wage growth remains elevated, projected at 6% for 2026, which continues to support private consumption. Household saving rates remain high, exceeding 16%, suggesting consumer caution in the face of geopolitical and economic uncertainty.

The pivot toward pro-growth monetary-fiscal coordination in Hungary

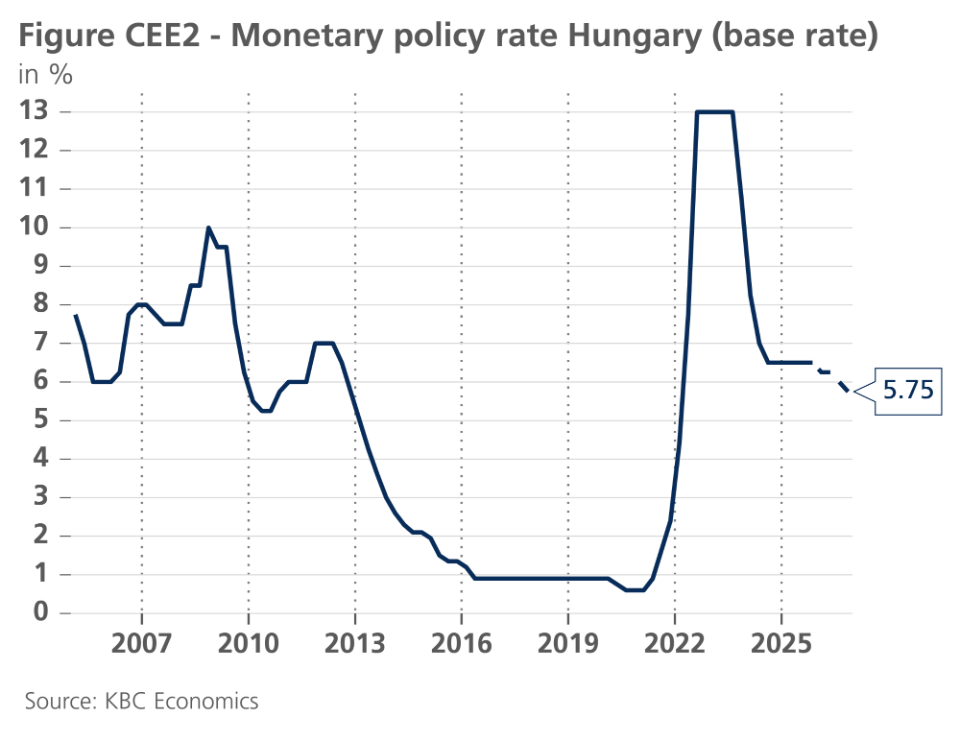

In February the MNB reduced the base rate by 25 basis points to 6.25%, marking the first cut in eighteen months (see figure CEE2). This policy shift was enabled by a sharp disinflationary trend: February 2026 inflation fell to 1.4%, confirming our nowcast, but undershooting market expectations and reaching an almost eight‑year low. We expect average Hungarian HICP inflation to reach 3.2% this year and 3.5% in 2027.

Governor Varga emphasized a "data-driven, cautious, patient approach" noting that the MNB does not have a pre-announced rate path and remains vigilant against energy price shocks and forint volatility. We anticipate a further 50 basis points of easing in 2026, with the base rate likely standing at 5.75 % by year-end.

The Hungarian government has leveraged the early months of 2026 to promote its "anti-war, family-focused" budget. The budget deficit for 2026 is now projected at 3.7% of GDP, a level that significantly exceeds the EU’s 3% threshold but lags behind our own forecast of 5.5%. The Fiscal Council has noted that this deficit is primarily sustained by lower interest expenditures as inflation-linked government bonds should reprice at lower rates.

The Hungarian economy continues to exhibit a "duality" where robust retail sales and services, supported by rising real wages, contrast with a subdued industrial sector. Industrial production remains under pressure from persistent consumer pessimism and volatile investor sentiment. However, capacity-increasing projects by BYD and BMW are expected to move into mass production later in 2026, which is anticipated to translate previous investment flows into measurable output and export volumes. Even then, we predict this year´s average GDP growth will stay below the government’s ambitious 4.1% target at only 1.9%. Our projection for 2027 growth is more optimistic at 2.9%.

Balancing fiscal consolidation and industrial fragility in Slovakia

In early 2026, the Slovak government continued the implementation of its multi-year consolidation plan, aimed at reducing the fiscal deficit to below 3% of GDP by 2027. The measures adopted are projected to have a contractionary impact on private consumption throughout 2026. We expect real GDP growth to reach 0.8% this year, the same rate as in 2025. A slight growth acceleration, to a 1.3% annual average rate, is expected in 2027. The weak aggregate performance is caused by two major factors: the direct impact of higher taxes on disposable income and the indirect effect of trade uncertainty on Slovakia's automotive sector.

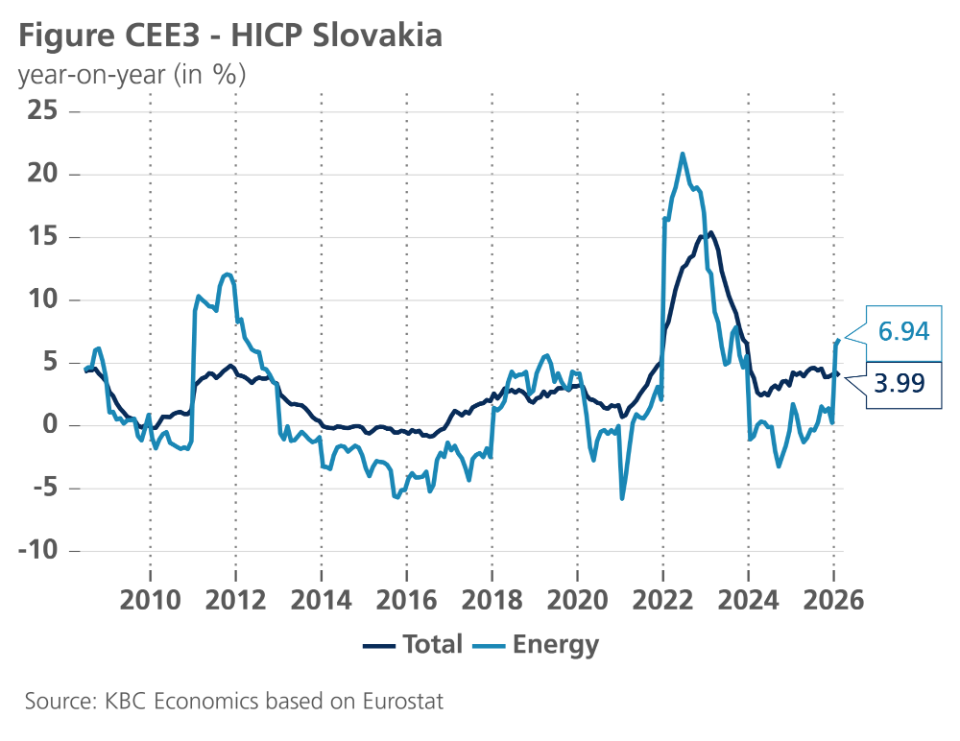

Slovakia’s inflation rate remains elevated compared to its peers, primarily due to the withdrawal of energy price ceilings and the impact of the VAT increase. In January, year-over-year inflation hit a four-month high of 4.3%, driven by a 25% surge in thermal energy prices. A month later, headline inflation decelerated slightly to 4% (see figure CEE3). We expect Slovak average HICP inflation to reach 4.1% this year and 3.1% in 2027.

The Slovak labour market remains resilient but is beginning to show signs of cooling. The unemployment rate at the end of 2025 was 5.6%, and we expect it to rise marginally to 5.9% by the end of this year as increased taxes and reduced public sector wage growth weigh on hiring dynamics. Real wage growth is projected to turn negative in 2026 as inflation outpaces nominal increases.

Slovak industry experienced a rebound in January 2026, with industrial production rising 2.7% year-on-year after three consecutive months of declines. This recovery was broad based, with 11 of 15 monitored industrial sectors recording growth. Despite this production rebound, the external balance remains fragile. Slovakia's exports fell 2.8% during the month. The drop was most pronounced in shipments to non-EU countries, which tumbled by 18.3%, highlighting the vulnerability of the Slovak automotive industry to non-European markets.

The euro adoption milestone and post-integration stability in Bulgaria

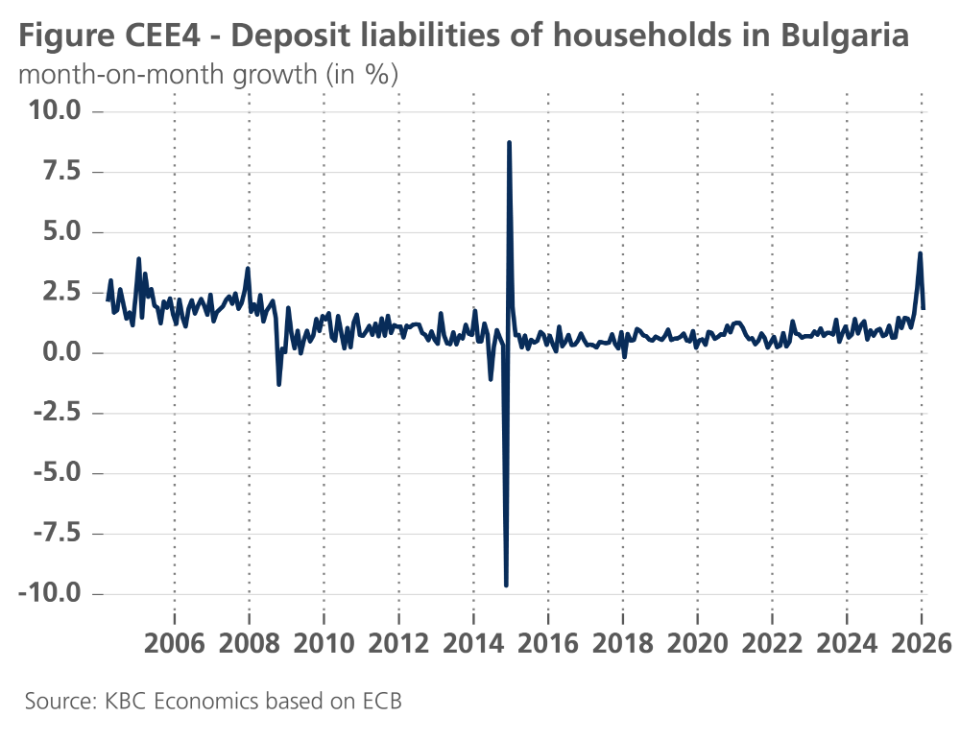

The first two months of 2026 have been a landmark period for Bulgaria, as the country successfully integrated into the euro area on January 1. By the end of the dual circulation period on January 31, 2026, the transition from the lev to the euro was deemed technically smooth. Bulgarian residents have continued to deposit lev cash for automatic conversion, leading to an acceleration in the growth of non-government sector deposits (see figure CEE4). By mid-March 2026, 89% of the total lev cash in circulation had been withdrawn from the market. To allay public concerns about price gouging, the authorities have maintained a rigorous monitoring regime, with the mandatory dual display of prices scheduled to continue until August 2026.

Bulgaria's inflation rate has remained relatively stable during the transition. February 2026 CPI inflation stood at 3.3%, with a monthly increase of 0.4%. HICP inflation showed a lower year-over-year rate of 2.1%. We expect average HICP inflation to reach 3.7% this year and 2.4% in 2027.

The industrial sector has faced a significant contraction, plummeting by 8.6% year-on-year, the largest decrease in the region. This decline reflects the broader "first-round" impact of US tariffs and the cooling of demand in major European export markets. Nonetheless, Bulgaria's GDP is projected to grow by 2.7% in 2026 and 2.8% next year, driven by real labor income growth and increased absorption of EU funds.

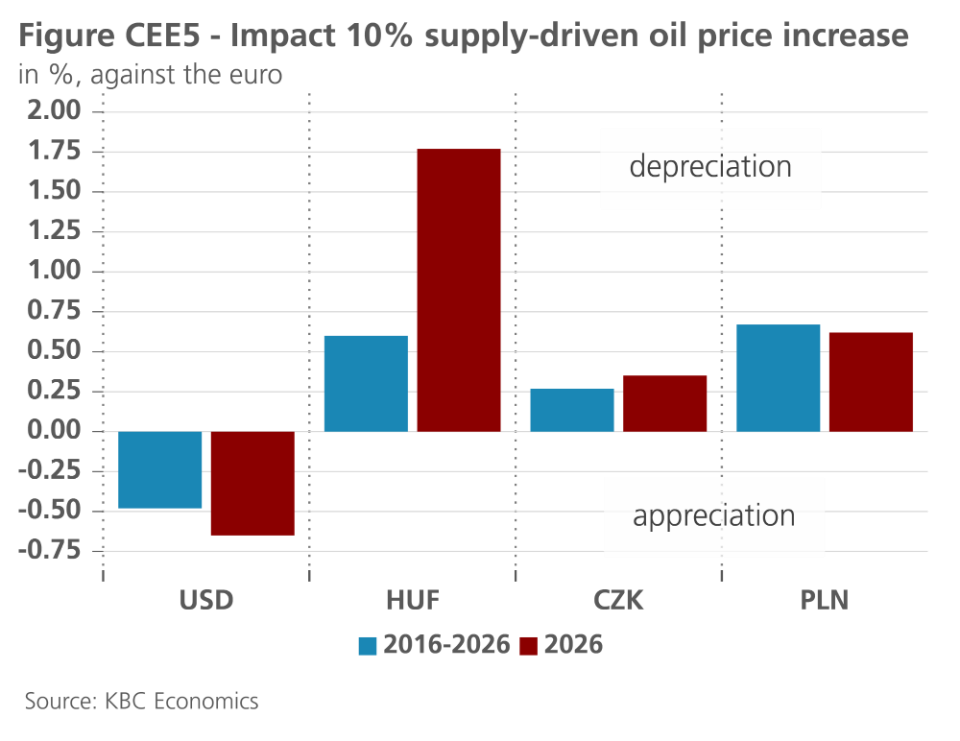

Box 1 – HUF especially sensitive to oil supply shocks

The energy supply shock has a major impact on currencies worldwide. Figure CEE5 shows impulse response functions of exchange rates on the day of impact to a negative oil supply shock.2 For the USD, higher oil prices increase demand for the dollar, given the US's status as a net energy exporter, resulting in appreciation against the euro. The estimated median response shows a 0.5% USD appreciation for a 10% oil price increase. This mechanism was one of the important drivers of dollar appreciation in 2026. For CEE currencies, which belong to energy-importing economies, the estimates show additional depreciation against the euro, reflecting higher energy pass-through to CPI and the market's assessment of central banks' ability to manage inflationary pressures. The additional depreciation is around 0.25% for the Czech koruna and 0.65% for the Hungarian forint. Risk-off mechanisms may add further pressure.

Re-estimating the model using only 2026 data, rather than the full sample from 2016, the impact increases slightly for all currencies, reflecting non-linearities caused by the magnitude of the current crisis. For the forint, however, the reaction more than doubled. Several Hungary-specific factors explain this outsized sensitivity. A fiscal deficit around 5% of GDP with elevated financing needs and economic growth below CEE peers make it more difficult for the MNB to raise rates to deal effectively with potential inflation increases. Moreover, Hungary has done little to diversify away from Russian crude, with reliance rising to roughly 86%, making it uniquely exposed among EU members. This vulnerability was compounded by the disruption of the Druzhba pipeline in late January 2026, which severed Hungary's primary supply route weeks before the Iran war sent global prices surging. Taken together, these factors potentially make the pass-through of the energy shock to Hungarian CPI more severe than in the rest of the region.

Footnotes

1/ BVAR model identifying structural shocks, inspired by Ferrucci, Gianluigi, Rebeca Jiménez-Rodríguez, and Luca Onorante. ‘Food Price Pass-Through in the Euro Area—The Role of Asymmetries and Non-Linearities.’ (2010).

2/ Oil supply shocks are identified using a Bayesian SVAR with sign restrictions on daily market data. The identification scheme requires a negative oil supply shock to raise oil prices, increase market inflation expectations, and lower stock prices excluding the energy sector.