Impact of the recent rise in energy prices

Click here to open the PDF.

On Saturday 28 February, the US and Israel started operation “Epic Fury”, launching multiple strikes on targets in Iran. Ayatollah Khamenei along with other high-level government officials and military leadership were killed during the strikes. Iran reacted by launching missiles towards Israel, American allies and US bases. Increasingly, oil infrastructure, both in Iran and across the Middle East are being targeted. Iran also threatened to close the Strait of Hormuz, a crucial chokepoint for oil and gas flows. Though it hasn’t done so yet, shipping through the Strait of Hormuz has declined to a near standstill. Though Donald Trump declared that the war will end “soon”, there is still significant uncertainty regarding how this conflict will evolve. The longer it lasts and the further it escalates, the larger the impact will be on global economic developments. The main channels of impact include higher energy prices, higher shipping costs, higher fertilizer prices (impacting global food prices) and aluminum prices, disrupted supply chains, and negative impacts on business and consumer sentiment due to elevated uncertainty.

Impact on energy markets

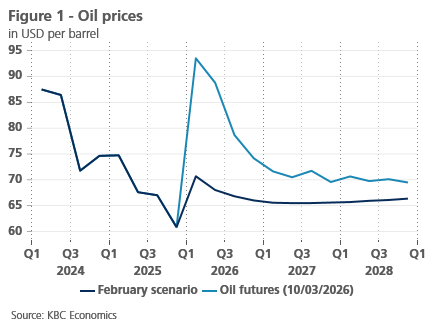

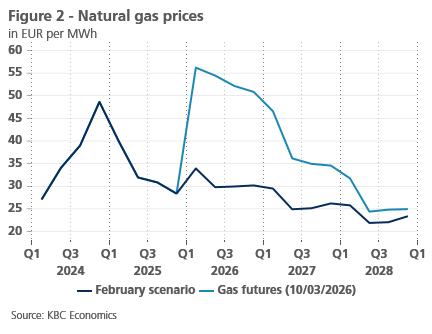

The largest economic impact will stem from energy price increases. Energy markets remain highly volatile, but oil prices have increased 32% relative to our February scenario (see figure 1), while TTF natural gas prices have risen by more than 67% (see figure 2). Futures markets see smaller increases, indicating markets expect the situation to normalise in the medium term. However, further escalation could put additional and major upward pressure on oil prices. The Middle East provides around 30% of global oil production and 17% of global natural gas production. Around 20% of global oil supplies and global LNG flow through the Strait of Hormuz. Iran itself supplies 4.5% of global oil production and 7% of global natural gas production.

Economic impact

The recent rise in oil and gas prices is likely to have to a modest negative impact on growth for both the US and European economies, given the temporary nature of the shock (according to the futures). It is also important to note that the European and US economies have become much less oil and gas-intensive in recent decades, making the economy more resistant to energy shocks. That said, if energy prices were to rise higher and stay higher for longer, the shock to the economy would become more serious.

The current energy price increases are likely to have a more important impact on inflation. This is especially the case for the euro area, where natural gas prices have risen substantially. In the US, where the natural gas market is largely domestic, prices have remained under control. Indeed, inflation expectations for the next 12 months have risen faster in the euro area than in the US (see figure 3). Long-term inflation expectations remain well-anchored for now.

Consequences for central banks

The stagflationary nature of the current energy price shock puts central banks in a bind. The immediate inflationary impact of the current shock will keep inflation above target in the US and drive it above target in the euro area. However, many central banks will be reluctant to tighten monetary policy sharply in response to the shock, given the downside risks for growth and employment. Nonetheless, markets now expect only one Fed rate cut this year (down from two before the war). This shift happened despite a benign inflation report and despite a poor employment report (showing 92k job losses in February). For the ECB, markets now expect two rate hikes this year. As mentioned above, this is likely because of the higher inflationary impact in the euro area. It is important to stress the high uncertainty here. Were oil and gas prices to spike even higher and were the shock to become more permanent, central banks could adopt a more hawkish stance.