Why US CPI and PCE inflation figures diverge

US PCE inflation has outstripped CPI inflation in recent months (in contrast to historical trends). This was especially the case for core inflation. The divergence is caused by important weight differences between PCE and CPI inflation. As CPI measures price changes directly paid for by consumers, housing and vehicle prices have a higher weight in CPI inflation. In contrast to CPI inflation, PCE inflation is broader and measures price changes of goods and services consumed (though not necessarily directly paid) by consumers. Items such as medical care services, financial services and software thus have higher weights. Especially the latter has seen high price rises in recent months. Looking ahead, core CPI & PCE inflation could continue to diverge as rent inflation is expected to moderate while software prices could accelerate further.

How high is US inflation? The answer to this question depends on who you ask. Consumers and market participants will typically refer to CPI inflation figures. This inflation gauge is used for inflation-linked contracts and for cost-of-living adjustment to reprice a.o. wages and social security adjustments. In contrast, policy makers, in particular the Federal Reserve, look at PCE inflation. To fulfill one part of its dual mandate, i.e. the price stability mandate, the Fed aims for PCE inflation to be around 2% over the longer run.

Methodological differences

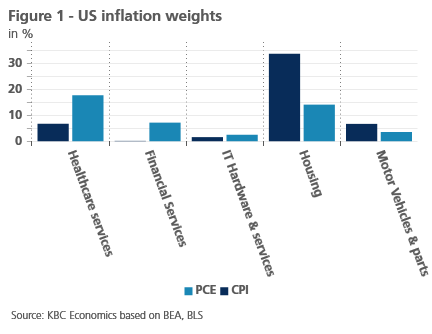

There are important methodological differences between PCE and CPI inflation. CPI inflation measures average changes in prices directly paid by urban consumers. In contrast, PCE inflation measures price changes of goods and services consumed (though not necessarily directly paid) by consumers (both urban and rural ones). That is an important difference and results in important weight differences between PCE and CPI. Healthcare, which is often paid for by employers or by the government, has a much higher weight in PCE than CPI (see figure 1). The same is true for financial services, where CPI only includes out-of-pocket fees and commissions, while PCE also includes imputed costs for financial intermediation. Software also has a higher weight in the PCE, as many software subscriptions used by consumers are paid for by employers (e.g. Microsoft 365 subscriptions). In contrast, in the CPI index, goods and services that are directly paid for by consumers (e.g. rent and automobiles) carry a higher weight.

It is also important to note that the CPI calculations are mostly based on household surveys and retail price sampling (i.e. the Consumer Expenditure Survey), while the PCE relies more on business surveys and administrative data. This causes some underweights in the CPI basket as consumers frequently underestimate what they pay for certain items (e.g. software subscriptions).

Another important methodological difference is that CPI weights are only adjusted annually, while PCE weights are adjusted dynamically (based on consumer spending data) and thus change at every release. When the price of an item rises fast, customers tend to spend less on it, which lowers its weight in their spending basket. Given its dynamic weight adjustments, the PCE better captures this effect.

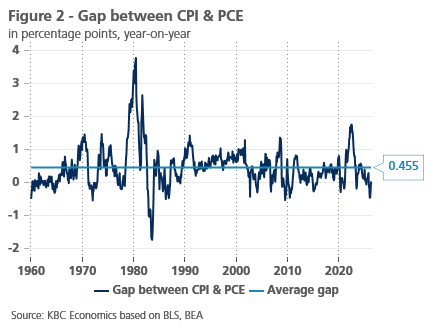

Partly because of this reason, PCE inflation tends to be lower than CPI inflation historically (see figure 2). Another reason is the rapid rise in housing costs, which far outstripped overall inflation in recent decades.

PCE outstripped CPI recently

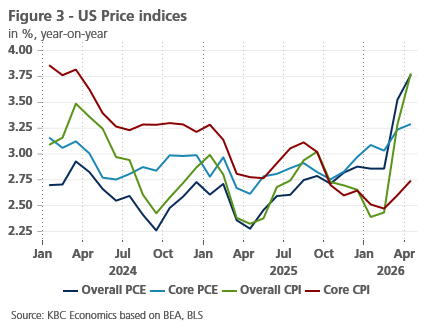

Yet more recently, PCE inflation outstripped CPI inflation (see figure 3). In February, PCE inflation was 0.46 percentage point higher than CPI inflation. That gap disappeared in the next two months as both CPI & PCE inflation reached 3.8% in April. However, core PCE (at 3.3%) remained far higher than core CPI (at 2.7%). Indeed, the main reason why headline CPI caught up with headline PCE inflation was the sharp rise in energy inflation (which has a higher weight in CPI inflation).

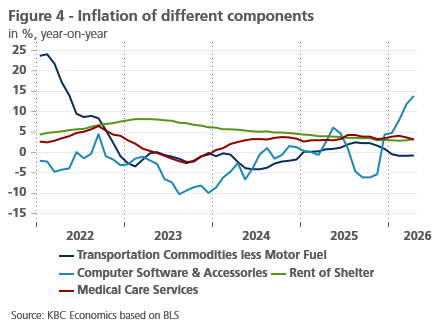

So why is core PCE so much higher? The explanation again lies in weight differences. Some components with higher weight in PCE have accelerated recently. Software prices in particular have accelerated significantly, because of the current AI boom. In contrast, vehicle prices and rent (whose CPI weight is higher) have decelerated in recent years (see figure 4).

Will the divergence last?

Whether PCE inflation continues to outstrip CPI inflation is highly dependent on the war in Iran. Were the conflict to end soon (as indicated by oil futures), we can expect energy prices to drop. This would push CPI inflation down faster than PCE inflation. A longer closure of the Strait would have the opposite effect.

For core inflation, we can expect the divergence to last in the coming months. The AI boom seems to continue unabated, pushing up prices for IT-related items. Meanwhile, shelter inflation (by far the largest CPI component) is likely to moderate further in the months ahead as indicated by market rents. Higher vehicle prices (as indicated by forward-looking indicators) could provide some compensation, but are unlikely to close the gap.