Prices on EU housing market continued to rise in Q1 2026, but country differences remain large

Click here to open the PDF

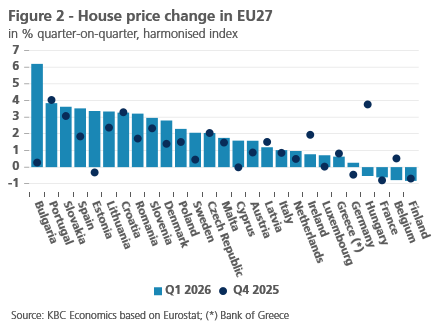

According to new Eurostat figures, prices on the European housing market continued to rise in the first quarter of 2026. The quarterly rate of increase in prices even strengthened, from 0.7% to 1.2%. The year-on-year growth momentum slackened slightly, but remained slightly above 5%. There were again significant differences between member states. In four countries (the same number as in Q4 2025), prices fell compared to the previous quarter, albeit by less than 1%: Finland, France, Belgium and Hungary. In eight countries (twice as many as in Q4 2025), the price increase exceeded 3%: Romania, Croatia, Lithuania, Estonia, Spain, Slovakia and Portugal, with Bulgaria (+6.2%) as the outlier. In Belgium, the general fall in prices (-0.8%) concealed a split development, with the prices of existing homes rising further (+1.3%) but those of new homes falling sharply (-6.5%).

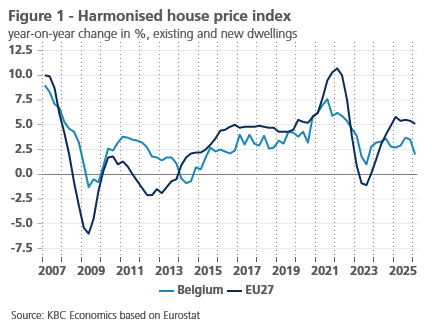

Eurostat recently published house price figures for the first quarter of 2026. This is the harmonised house price index for EU member states, which takes into account both existing and new homes and corrects for price changes due to changes in the characteristics of the property sold. In the EU as a whole, house prices rose by 1.2% in Q1 2026 compared to the previous quarter. This is an acceleration of quarterly price dynamics compared to Q4 2025 (+0.7%), when the rate of increase had weakened compared to that in the three previous quarters of 2025 (around 1.5% each). Compared to the same quarter a year earlier, house prices in the EU were 5.1% higher in Q1 2026. The year-on-year increase was slightly lower than in the four quarters of 2025 (see figure 1).

Country differences

In Q1 2026, there were four countries (Finland, France, Belgium and Hungary) where house prices fell compared to the previous quarter (see figure 2). The price decrease was limited to less than 1%, though. In Finland and France, the correction was a continuation of a price decline in Q4 2025. In both countries, the housing market continues to suffer from weakness and the price level in Q1 2026 was still 14.3% and 5.8% respectively below the previous peak in 2022. In Luxembourg, Germany and Sweden, which also had to deal with a sharp correction earlier, the price level in Q1 2026 was also still below the peak in 2022 (by 14.1%, 8.4% and 4.3% respectively), but the market there is now recovering with positive price figures in Q1 2026 as well.

The Q1 price drop in Belgium and Hungary stands out. In Belgium, this follows a recovery in price dynamics after only a limited cooling of the housing market at the end of 2022-beginning of 2023. House prices in Q1 2026 were again 8.1% above the peak in 2022 (for the EU as a whole it is 10.4%). Apart from the negative Q1 2026 figure, Hungary has only had one other negative quarterly figure in recent years (Q4 2022), which was followed by consecutive strong quarterly figures. In Q1 2026, house prices in Hungary were no less than 52% higher than in 2022.

In eight EU countries, quarterly house price growth in Q1 2026 was more than 3%. That is twice as many as in Q4 2025. In Romania, Croatia, Lithuania, Estonia, Spain, Slovakia and Portugal, the quarterly price increase in the first quarter was 3 to 4%. Bulgaria was the outlier with a price increase of 6.2%. With the exception of Estonia, these are countries where price dynamics have also been particularly strong in (most) previous quarters and where there has been little or no cooling of the housing market in the past.

Compared to the same quarter a year earlier, only one EU country, Finland (-2.0%), showed a decline in house prices in the first quarter of 2026. The highest annual price increase was recorded in Portugal (+17.8%). Eight other Eastern and Southern European countries also recorded double-digit annual price increases in Q1 2026: Bulgaria (+14.8%), Slovakia (+14.4%), Croatia (+14.3%), Spain (12.8%), Lithuania (+11.9%), Latvia (10.9%), Hungary (+11.2%) and the Czech Republic (+10.1%). For your information: house prices in Belgium were 2.0% higher in Q1 2026 than a year earlier, implying a slight slowdown in year-on-year growth dynamics compared to previous quarters (see figure 1).

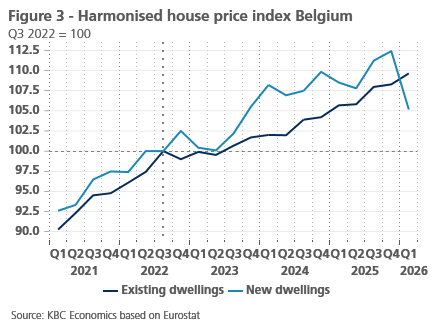

Existing versus new homes

For the EU as a whole, the price increase of existing homes (+1.2%) and new homes (+1.1%) in Q1 2026 was not very different. Similarly, for most Member States, price dynamics for existing and new homes have been fairly parallel (i.e. strong or weak for both segments). There are a number of notable exceptions. In five countries (Latvia, Luxembourg, Italy, Hungary and Belgium), prices for existing homes rose but fell for new ones in Q1 2026. The difference was largest in Hungary (+0.2% for existing and -7.0% for new ones) and Belgium (+1.3% for existing and -6.5% for new ones).

The sharp fall in the price of new homes in Belgium in Q1 2026 offset the relatively stronger price increase in recent years compared to that of existing homes (see figure 3). The price development of new homes is generally more volatile than that of existing ones, with also a few quarters of price decline in recent years, although not as strong as in Q1 2026. We think that the weaker Q1 figure is not a harbinger of further price corrections. The fundamentals of Belgian real estate are not bad and, moreover, the market is no longer overvalued, at least according to the KBC valuation model. Nevertheless, we have adjusted our forecast for the general price development of Belgian real estate in 2026 somewhat downwards. For the whole of (existing and new) homes, we now assume an average price increase of around 2% in 2026 (coming from 3% in our earlier forecast). With headline inflation at around 3%, this house price forecast for 2026 does imply a real house price decline (i.e. adjusted for HICP inflation) of around 1%.