Tariff ruling: ST pain, LT gain?

The US Supreme Court recently ruled that the Trump administration cannot issue tariffs based on the International Emergency Economic Powers Act. This upends Trump’s current trade policy, as a majority of his tariffs are based on this ruling. The administration has other options. Following the ruling, Trump issued a blanket 15% tariff based on Section 122. As many countries faced higher tariffs than 15% before the ruling, the US effective rate tariff rate dropped from 16% pre-ruling to 13.7% post-ruling. In the future, the administration is likely to use a combination of Section 301 and 232 tariffs to bring tariffs back close to original levels (both require lengthy investigations). Though eventual tariff reimbursements and lower short-term effective tariff rates could provide a boost to the US economy, potential upsides are likely to be outweighed by the negative effects of higher uncertainty. That said, as the ruling constrains this administration and futures ones, US trade policy is likely to become more predictable in the longer run.

On 20 February, the Supreme Court finally issued a ruling in “Learning Resources v Trump”. The case revolved around whether Donald Trump could use the International Emergency Economic Powers Act (IEEPA) to set tariffs. In a 6-3 ruling, the Supreme Court ruled against the use of this law to impose tariffs on other countries. The Court noted that the constitution “gave Congress alone the power to impose tariffs during peacetime” and “did not vest any part of the taxing power to the executive branch”. As IEEPA only allows the president to regulate imports (and does not mention the word tariffs), it thus cannot be used to impose tariffs.

The decision is a blow to Donald Trump’s trade agenda. Most of his tariffs were based on IEEPA. Indeed, according to the Yale Budget Lab, the average effective tariff rate dropped from 16% to 9.1% immediately after the ruling. Though the Supreme Court ruling didn’t include a decision on reimbursements, many businesses will now be able to sue the government for tariff reimbursements. An estimated 175 billion USD was collected through IEEPA and could be reimbursed. These reimbursements, if received, would provide a mild stimulus to the economy, but would also exacerbate US budgetary issues.

Other options: Section 122

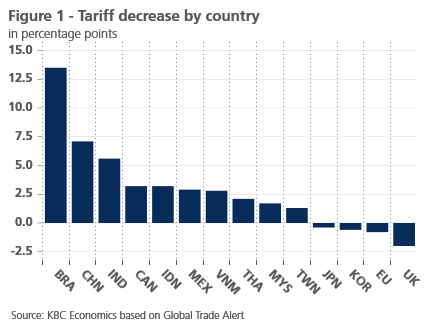

Though the ruling constrains Trump’s trade policies, the president has other options to impose tariffs without the need for congressional approval. He almost immediately invoked Section 122 from the 1974 Trade Act to impose a 10% global tariff. He announced a raise the day later to 15%. Section 122 allows Trump to impose tariffs on all countries to address balance of payments needs or to prevent a significant depreciation of the dollar. Section 122 comes with constraints, however. Congressional approval is needed after 150 days. Furthermore, 15% is the maximum percentage Section 122 allows to charge. As many countries faced higher tariff rates before the ruling, they will be pleased to see their effective tariff rate drop (see figure 1). Some countries such as the UK had faced a lower tariff before and will see a slight tariff increase. The effective tariff rate for the EU will also increase as fewer goods will be exempt from the 15% rate. Overall, as many countries see their tariff rates drop for now, the effective tariff rate falls from 16% before the ruling to 13.7% today.

Next options: Section 301 and 232

Though countries such as Brazil and China will be pleased to see their effective tariff drop, their relief is likely to be short-lived. The US administration is likely to use other options to bring effective tariff rates close to pre-ruling levels. Most likely is the usage of Section 301 from the 1974 Trade Act (which it announced it intends to do on most major trading partners). This allows the Trump administration to impose tariffs on a trading partner that has gained an “unfair advantage.” However, to impose it, a lengthy and cumbersome investigation normally needs to be done. In the first Trump administration, the investigation into China lasted more than six months.

On top of Section 301 tariffs, the administration will continue using Section 232 tariffs from the 162 Trade Expansion Act. These are tariffs that can be used to protect sectors where imports threaten national security (and also need investigations). They are already used for the car industry, steel & aluminum, kitchen cabinets, and upholstered furniture. Other sectors such as semiconductors are under investigation.

Economic consequences

The ruling will have a few economic consequences. First, as we mentioned there could be a mild stimulative boost from the tariff reimbursements. Second, the lower effective tariff will also likely be stimulative to US growth and lower US goods inflation. That said this effect is likely to be small as the effective tariff only declined by 2.3 percentage points. The drop is also likely to be short-lived as new Section 301 and Section 232 tariffs are likely to be imposed in the coming months.

The small positive economic boost from possible tariff reimbursement and temporary lower effective tariff rates is likely to be outweighed by the negative effect of continued trade policy uncertainty caused by this ruling. Indeed, as we argued last year (see Economic Opinion of 10 February 2025), tariff uncertainty can be as damaging as the direct effect of tariffs themselves as the uncertainty deters investment.

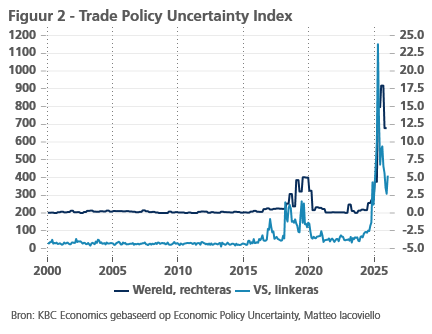

Following Liberation Day, trade uncertainty rose to an unprecedented high (see figure 2). Though it eased since, it remains at very elevated levels. The current ruling will keep uncertainty elevated in the coming months as the administration will gradually announce new Section 301 and Section 232 tariffs and several trade deals will have to be renegotiated.

That said, on the longer run, the Supreme Court’s ruling will lower trade uncertainty. As this administration (and future ones) cannot announce tariff increases on a whim anymore (given the need for investigations in Section 232 and 301), US trade policy is likely to become more predictable. This will eventually give investors some more certainty after a year of erratic trade policy making.