Iran: economic pearl of the Middle East doesn’t shine due to political conflicts

The direct confrontation between the US and Iran fuels fears that a new and escalating conflict in the Middle East will disrupt the global economy. For the time being, financial markets remain calm and the economic impact seems limited. Against the background of the conflict, the Iranian economic situation is playing out. Iran suffers enormously from international sanctions which prevent it from realizing its potential. Nevertheless, Iran has a number of strong economic assets and a remarkably resilient economic performance thanks to sound economic policies. A renewed dialogue with the West could potentially lead to significant economic prosperity for the Iranian people and new opportunities, especially for European companies. This seems a valuable alternative to the current geopolitical confrontation.

Up and down

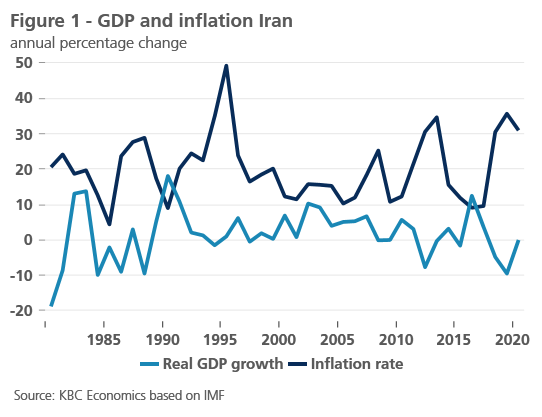

Since the Iranian revolution, Iran has had a difficult economic trajectory. International sanctions prevented Iran from enjoying the prosperous economic developments seen elsewhere in the region. The international nuclear agreement of 2016 gave the Iranian economy a strong boost in 2016 and 2017, after years of sanctions, deep and rapid economic reforms allowed Iran to flourish economically, almost instantly. Unfortunately, the economic recovery was short-lived. After the reintroduction of US sanctions, the Iranian economy collapsed again. The new, additional US sanctions, following the Iranian missile attack on US military installations in Iraq, will further hurt the Iranian economy.

Iran can best be described as an emerging economy pushed into developing country status by international conflicts. The country owes its status as an emerging economy to a number of economic assets that should, in principle, allow it to achieve high economic growth and fast development. This is evident from the rapid but unfortunately short-lived upturn in all macro-economic indicators following the signing of the nuclear agreement in 2016. Real economic growth (Figure 1) accelerated immediately, while inflation fell. The aforementioned assets include its strategic geographical location, its size (83 million inhabitants), its relatively well-educated population, a relatively market-based economy, and its financial buffer from oil (and gas) revenues.

IMF compliments

The Iranian government has even been praised by international institutions, such as the IMF, for its successful economic policy based on sound economic principles. A good mix of monetary and fiscal stimulus, with an explicit focus on strengthening economic activities outside the oil sector, supported the economic upturn in 2016 and 2017. This is not surprising as historically, Iran has a tradition of a differentiated economy, unlike many other Arab countries. This is reflected in its diversification of exports to petrochemical products and food, among other things. During the 2016-2017 upturn, important steps were taken in terms of institutional stability, regulatory modernization and improved market access for domestic and foreign companies. The strong performance of the private sector during the upturn was also striking and so was the rapid rebound of the construction sector and service activities. The unemployment rate, while falling to 12% in 2017, is still high however and job creation and the inflow into the labour market should be stronger.

Uncertain and difficult future

Nevertheless, Iran faces a number of structural economic challenges. Above all, there is a need for much more foreign investment. Iran is, in principle, an interesting destination for foreign investors because of its many assets mentioned above. As a result, many companies, especially European ones, quickly took advantage of the new opportunities that presented themselves after the international rapprochement in 2016. In particular, international trade with Iran flourished, and to a lesser extent international investment too. Trade, of course, is a simpler and safer way to respond to the opportunities of the re-opening of the Iranian market than direct investments. And indeed, European interest in Iran melted like snow in the sun after the new American sanctions. In addition to a lack of foreign investors, Iran also lacks a stable financial sector that can structurally support growth. Recapitalization and reforms of Iranian banks is an essential first step. Further reforms are also needed in the area of monetary policy, with the abolition of the dual exchange rate system and greater independence for the central bank.

Of course, such challenges can only be tackled successfully in a stable geopolitical environment. As a result of rising tensions in recent years, the IMF expects a contraction of -9.5% in Iranian real GDP and an inflation rate of 35.7% in 2019. Until recently, a recovery was expected in 2020, but these estimates date back to before the recent US-Iranian conflict, so they are undoubtedly far too optimistic. The economic damage caused by the new sanctions and the current conflict will therefore be enormous. They are a disruption to the early recovery of the Iranian economy.

It is clear that Iran suffers from its weak economy, but at the same time it has the potential to be a very prosperous country. This makes the decades-long tense relationship with the West, and the current direct confrontation with the US, particularly regrettable. Few countries have assets similar to those of Iran. Unfortunately, those trump cards cannot be played out at the moment.