China’s internal imbalances are a global problem

- Read the publication below or click here to open the PDF.

Introduction

Protectionist trends in global trade dynamics extend well beyond Trump’s now-illegal tariffs. The Biden administration issued restrictions on chip exports, the EU has launched a record number of trade defence investigations in recent years, and many countries are frantically mobilising to reduce their critical raw material trade dependencies. At the centre of these trends is a long-simmering battle for technological and economic dominance between the reigning champion (the US) and the quickly advancing contender (China), while the other major economic power (the EU), finds itself unwillingly pulled into the ring. But this boxing metaphor assumes a transactional zero-sum view of global trade dynamics, in which China’s gain means another economy’s loss. For the EU, at least, there is some evidence of this, as the increased competition from Chinese manufacturing weighs on EU industries. It was once expected that China’s advancement up the economic ladder would unlock a vast market of eager consumers, supporting global growth more broadly, but this expectation has not yet materialised. China’s internal supply and demand imbalance is, therefore, an increasingly global problem, but one that requires a domestic solution.

China’s drivers of growth matter

Despite numerous headwinds, Chinese real GDP grew at a stable 5% average rate in 2025, thanks in large part to solid net exports. Consumption was more sluggish by historical standards, which is important in the context of China’s shifting growth model. The very high, state-directed infrastructure investment that drove Chinese growth for years, especially after the 2008 global financial crisis, is no longer tenable. The real estate crisis is part of this; much of the sharp drop in investments’ share of Chinese GDP (from a peak of 84% in 2009 to only 15% in 2025) is due to the pull back in investments in real estate and construction. But instead of consumption stepping up to fill the void, the gap has been bridged by stronger exports.

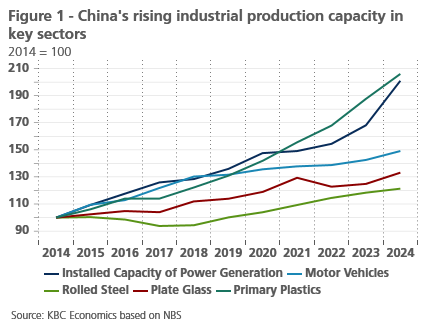

The composition of China’s growth has increasingly global consequences. Domestic demand is too weak to absorb the increased production capacity in specific industries (figure 1). This partly explains China’s export surge as producers look to markets abroad. It has also led to deflationary pressures within China, with producer prices negative in year-over-year terms since October 2022. These deflationary pressures help China’s lower cost exports cut into the market shares of competing industries.

China’s export resilience is more than trans-shipping

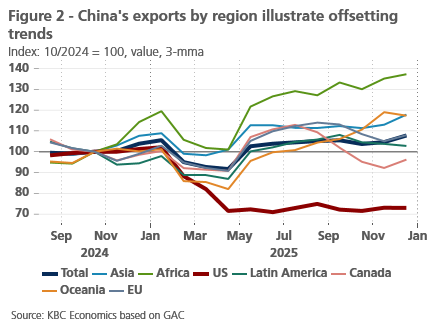

Despite China’s resilient export performance in 2025, higher tariffs imposed by the US had a clear negative impact on US-China trade. Chinese exports to the US have dropped substantially since April 2025 (figure 2). And although the May 2025 de-escalation between the two countries may have staunched the decline, Chinese exports to the US have not meaningfully recovered, even after a year-long trade truce was signed in October 2025. It might be tempting to suggest that the offsetting improvement in exports to other regions is merely a case of trans-shipping. I.e., Chinese producers are shipping to third countries, particularly in Africa, before sending them on to the US to avoid higher tariffs. But while US imports from Africa (on a rolling 12-month basis) grew at nearly the exact same pace as Chinese exports to Africa between November 2024 and June 2025 (+12.5%), throughout the second half of 2025, Chinese exports to Africa continued to grow sharply (+14%) while US imports from Africa levelled off and even declined (-2.45%). This suggests that, while trans-shipping may be playing a role, there is a deeper story to China’s export success.

Industrial upgrading boosts supply

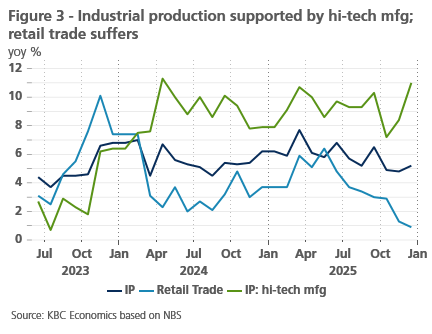

Industrial upgrading has long been a goal of the Chinese government. This means using targeted investments to move up the value chain in manufacturing, increase automation in the manufacturing sector, and support strategic independence in key, high-tech sectors (AI, quantum computing, semiconductors, green tech). This strategy is paying off. Industrial production has been a main driver of Chinese growth in recent years, particularly supported by high-tech manufacturing (figure 3).

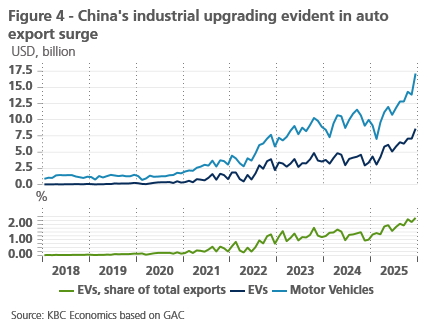

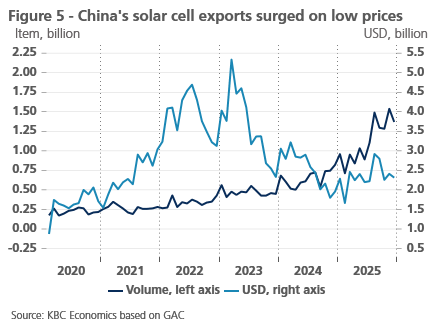

The increase in high-tech manufacturing is evident when looking at a breakdown of China’s goods exports. Take for example, China’s auto exports, which grew 285% since 2021. A significant portion of that growth has been thanks to electric car exports, which grew 362% over the same period (figure 4). We can see a similar trend in China’s export of solar cells, which, in terms of volume, grew 415% since the start of 2022 (figure 5). Over the same time horizon, the value of those solar cell exports (whether measured in USD or CNY), has declined slightly, highlighting that the low cost of China’s high-tech exports is playing a significant role in this export success.

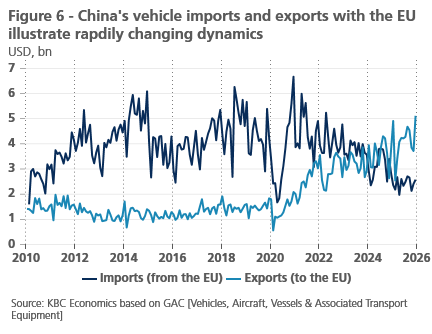

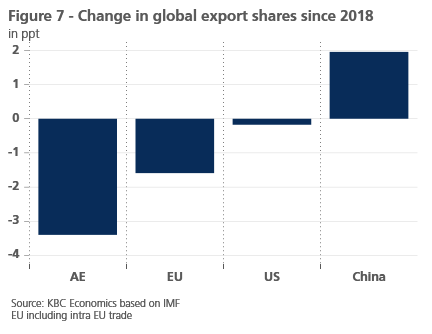

Low-cost exports from China have obvious implications for competing markets abroad. Europe’s car industry is a key example of this. Previously, the EU consistently exported more vehicles to China than it imported from China. However, starting in 2021, EU vehicle exports to China began to steadily decline, while Chinese vehicle exports to the EU steadily began to increase. The figures crossed each other in late 2023 and the gap continues to widen, meaning China now exports more vehicles to the EU than it imports from the EU (figure 6). This industry-specific phenomenon is evident from a wider perspective as well; since 2018, advanced economies have lost global market share for their exports while China has gained significantly (figure 7).

Demand side weakness

China’s widening trade surplus is not only about high external demand for Chinese products. As exports have surged, imports have flatlined. This is partly reflective of China’s policy push towards strategic independence (Made in China 2025)1, but also a reflection of weak consumer demand in China. Looking back at figure 3, its clear that while industrial production remained strong, retail sales have been extremely sluggish.

China’s household savings rate (as a share of disposable income) has long been much higher than that of other economies (35% in 2019 compared to 6% in the EU and 7.5% in the US). Like in other economies, savings surged even higher during the pandemic years. While many economies saw these extra savings at least partially unwind post-covid, Chinese consumers’ intentions to save have only moved higher. As of Q4 2025, 63% of consumers plan to save more going forward versus 46% six years ago, according to a consumer survey.

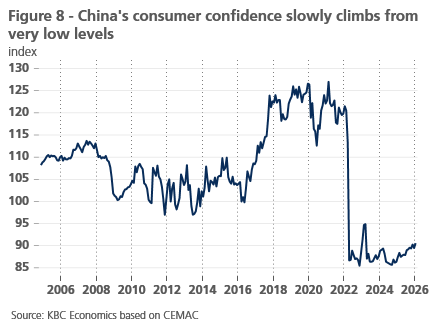

There are many explanations for China’s high savings and weak consumption, but gloomy consumer confidence plays an outsized role. Consumer confidence fell off a cliff in 2022 and has yet to recover (figure 8). The decline in confidence started already in 2021, coinciding with the start of the real estate sector downturn. As we’ve noted in previous research reports, significant household wealth in China is tied up in the real estate sector, and already elevated household mortgage debt is likely holding back consumption growth. The gloomy consumer confidence figure likely also reflects considerations regarding the labour market. The youth unemployment rate ended the year at 16.5%, while according to a PBoC survey, only 6.4% of respondents view the employment situation as “good”.

Conclusion: structural challenges require structural reforms

Rebalancing the Chinese economy will not be an easy fix. Traditional policy levers, like modest cuts to policy interest rates to induce demand, become less effective when households are deleveraging. And steps taken last year to fight deflationary pressures through so-called ‘anti-involution’ policies are weighing on investment growth and therefore GDP growth (fixed asset investment was down 3.8% in 2025 compared to 2024 – the first full-year negative figure in decades). Meanwhile, trade partners are growing increasingly wary of China’s growing market dominance in many industries, meaning that relying solely on external demand to power growth is not a sustainable long-term strategy.

In February, the IMF called on China to cut industrial subsidies and focus instead on supporting consumption driven growth. While this is part of the government’s latest Five-Year Plan, formally adopted this week, implementation will be key. After all, rebalancing the economy to become more services oriented while boosting consumer demand was also part of the last Five-Year Plan. So far, China has not adopted the right structural reforms to meet this long-standing structural problem.