Negative European bond yields not sustainable forever

On 22 March, the nominal German 10 year government bond yield became negative. As a result, German nominal yields are now close to the Japanese level. For some market participants, this has been a sign that the European economy is heading towards a ‘Japan’ scenario of ‘low forever’ interest rates in a stubbornly low inflation environment. In this Economic Opinion, we argue that this is not the case. Long term inflation expectations for the euro area are still substantially higher than for Japan. Given nominal bond yields at similar levels, this implies Japanese real yields are well above the strongly negative German real yield. In this regard, the euro area is the outlier, not Japan. The strongly negative real bond yield is mainly the result of the ECB’s exceptionally accommodative policy stance. As long as long-term inflation expectations in the euro area remain anchored in firmly positive territory, the question is not if, but when an upward normalisation of German nominal yields will eventually take place. Its precise timing is all but impossible to predict, but the US ‘taper tantrum’ experience in 2013 suggests that this could happen sooner than currently expected.

Negative once more...

For the first time since 2016, German 10 year nominal government bond yields turned negative again. This was partly the result of weaker than expected economic indicators, both globally and for the euro area. The main driving force, however, was a change in expectations for future ECB and Fed monetary policy. The latest Fed communication suggested that its rate hiking cycle may be over and that its balance sheet tapering is scheduled to end in September 2019. Meanwhile, the ECB made it clear that the first hike of its currently-negative deposit rate should not be expected before 2020. These lower-for-longer short-term interest rate expectations also further pulled down German long-term yields.

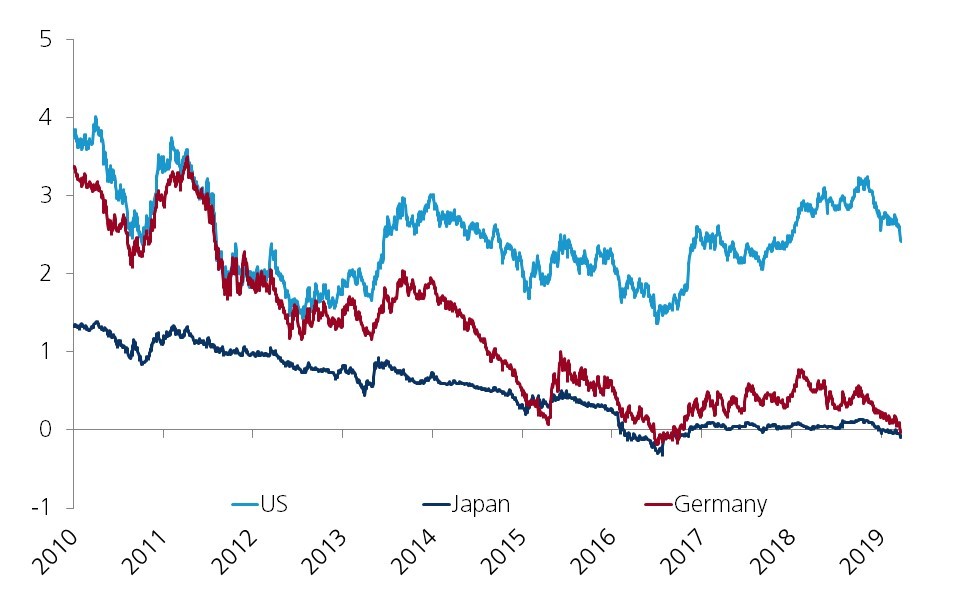

German bond yields are now only marginally higher than Japanese yields (see figure 1). At first sight, this could be interpreted to mean that the European economy is suffering from the same problem as the Japanese economy: low nominal yields reflect a weak growth environment in combination with an inflation rate that is well below the inflation target and even uncomfortably close to deflationary levels.

Figure 1 - German nominal bond yield drops to Japanese level (10 year government bond yields, in %)

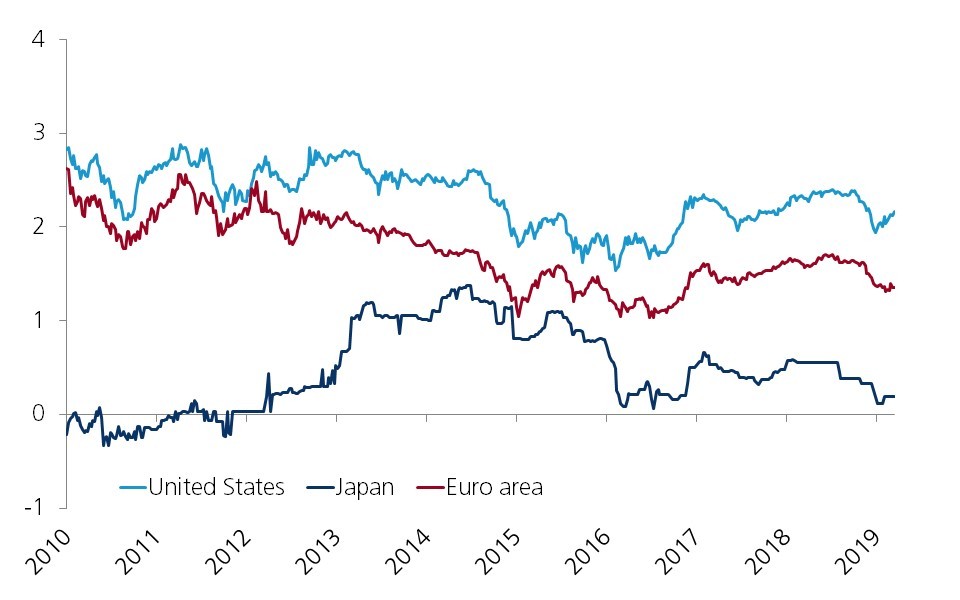

However, financial markets’ long term inflation expectations, as implied by inflation swaps, point to an important difference. In Japan, these inflation expectations remain well anchored close to 0%. For the euro area, on the other hand, they are significantly higher and slightly above the current underlying core inflation rate (see figure 2).

Figure 2 - Markets’ inflation expectations substantially higher for the euro area than Japan (based on inflation swaps, in %)

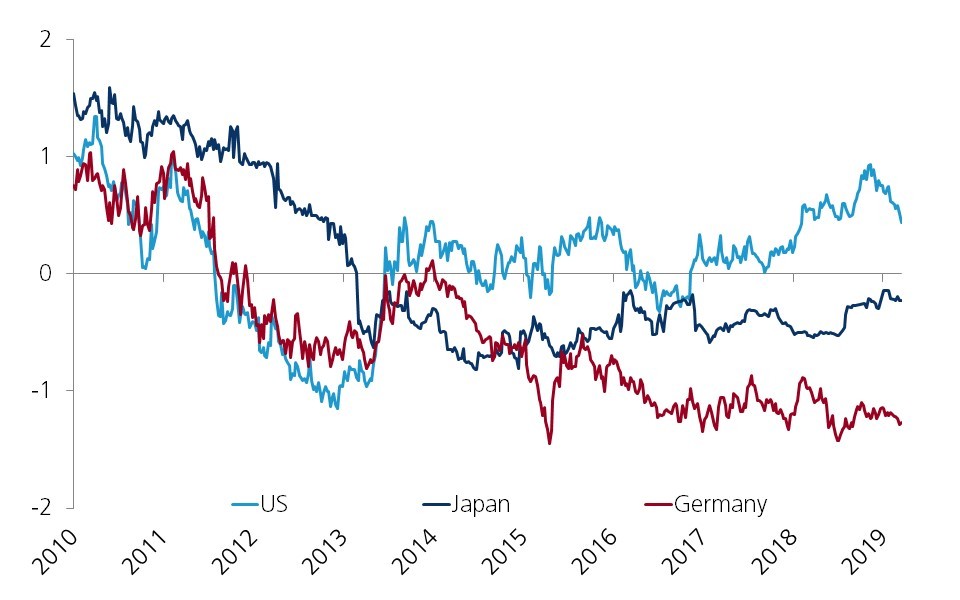

Combined with the same level of nominal bond yields, the higher rate of expected inflation implies that the real German bond yield is much lower (even significantly negative) than the corresponding Japanese real rate, which is close to 0% (see figure 3). This suggests that the euro area real rate is the outlier, well below the rate in both Japan and the US.

Figure 3 - Real bond yields strongly diverge (nominal yields minus inflation expectations, in %)

Artificial...hence ultimately unsustainable

Even with moderate growth and subdued inflation, the very fact that the European real bond yields are strongly negative suggests that they are not sustainable forever. The timing crucially depends on how long markets will be prepared to tolerate negative yields before demanding a higher nominal yield. Investors who hold German 10 year government bonds until maturity are certain to lose in real terms, and currently even in nominal terms. To illustrate this point: if German real yields rise to the same level as supposedly crisis-hit Japan, given current euro area inflation expectations, the nominal German yield would be about 100 basis points above its current level. If instead German real yields return to the current level of US real yields, the upward potential for German nominal yields would even be 170 basis points. This is not at all implausible if we keep in mind that US and German real yields moved closely in tandem until 2013, as a result of broadly similar nominal bond yields and inflation expectations. The subsequent divergence of mainly the nominal yields is a relatively recent phenomenon.

A major cause for the artificially low European bond yields is the ECB’s extremely accommodative policy stance. This is severely distorting the bond market in a way that cannot go on indefinitely. Paradoxically, interest rate markets are already taking this into account. The slope of the yield curve, as measured by the difference between the 10 year interest rate swap rate and the 3 month interbank rate, sends an interesting signal. The slope in the euro area is currently the steepest (about 80 basis points). In Japan, the curve is broadly flat (a slope of about 15 basis points) and outright negative in the US (minus 25 basis points).

Long term yields incorporate market expectations of future short term interest rates. In other words, the yield curve is not expecting the Bank of Japan to change its policy any time soon, while the Fed may even cut its policy rate. The ECB, on the other hand, is expected to actually raise its policy rate from its apparently unsustainably low level. That would ease the artificial downward pressure on longer term yields. However, as is always the case in economics, the precise timing is all but impossible to forecast.